Most people associate Android with phones. Maybe tablets. But over the last two years, something shifted in a market most consumers never see — the commercial kiosk and digital display industry. The self-ordering screen at a fast food chain, the check-in terminal at a hotel lobby, the wayfinding directory inside a shopping mall. Increasingly, those all run Android.

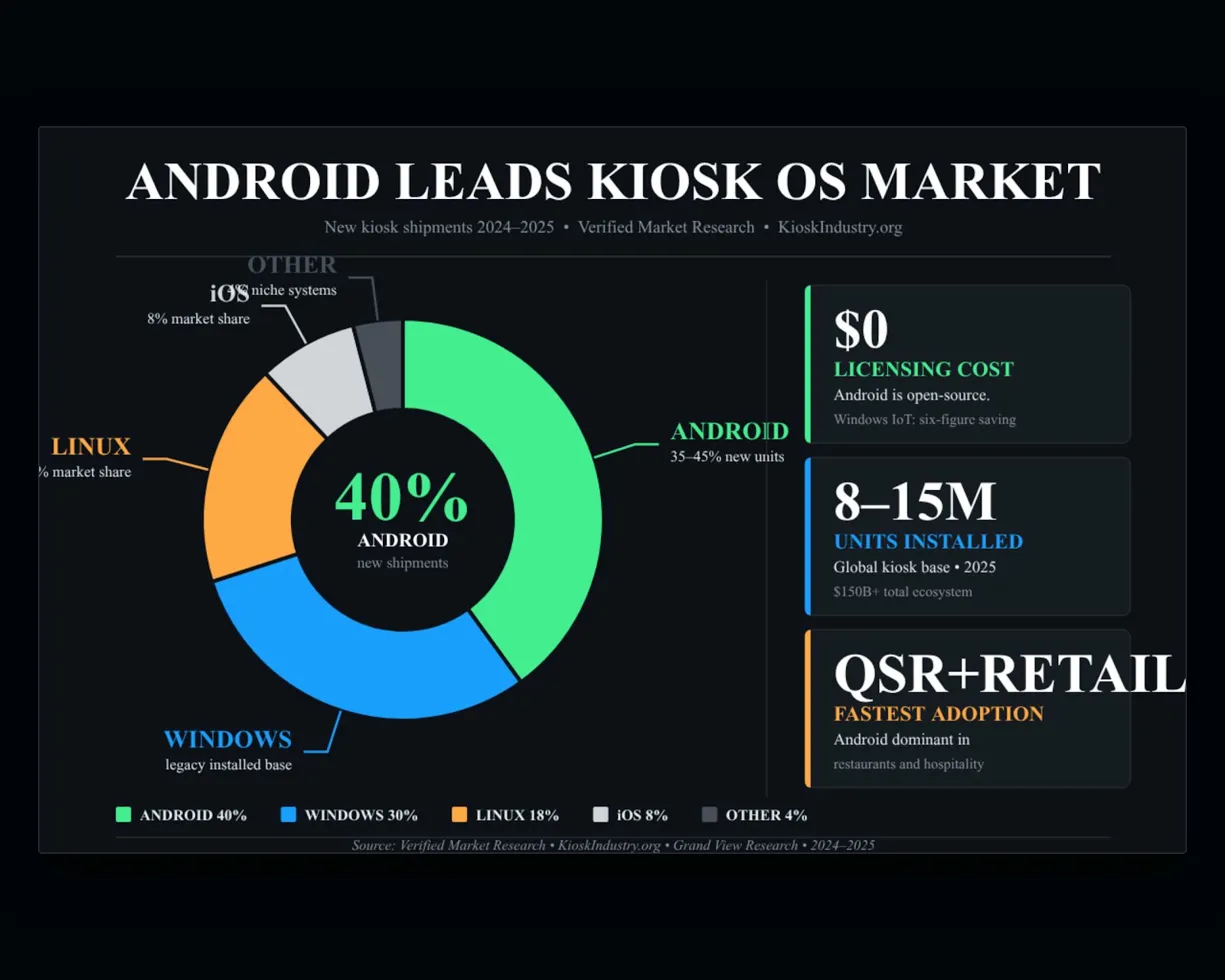

Multiple market analyses now confirm that Android holds the largest OS share in the kiosk operating system market, ahead of Windows, iOS, and Linux (Verified Market Research, Maximize Market Research). For new kiosk shipments in 2024-2025, Android is estimated at 35-45% of new units — sometimes higher in quick-service restaurants and hospitality (KioskIndustry.org).

The self-service kiosk market underneath this shift is valued at roughly $14.5-34.4 billion in 2024-2025 depending on which research firm and what they include in scope, with projections ranging from $25 billion to $62 billion by 2030 at growth rates between 10-15% CAGR (Grand View Research, Mordor Intelligence, Research Nester).

That’s the context. Here’s what actually happened recently that made this worth reporting.

LG showed up at ISE 2026 with a connected display ecosystem built for Android-scale deployment

In February 2026, LG Electronics took over a 1,184 square meter booth at ISE 2026 in Barcelona — their largest commercial display exhibition to date. The showcase wasn’t about screen resolution or brightness specs. It was about systems.

What they demonstrated:

- Transparent OLED panels for retail storefronts — product visible behind the glass, promotional content on the glass.

- Digital shelf displays with remote pricing and product info updates.

- Kiosks with QR/NFC smartphone handoff — public screen to personal device mid-interaction.

- LG Business Cloud — one centralised platform connecting every screen, kiosk, and display to remote monitoring, content scheduling, and analytics.

Park Hyoung-sei, president of LG’s Media Entertainment Solution Company, stated: “We’re redefining commercial spaces with integrated ecosystems that go beyond hardware.”

The reason this matters for Android specifically: cloud-managed, multi-device display networks are exactly where Android thrives. Low hardware cost per unit. Open app ecosystem. Remote device management through platforms like Google’s Android Enterprise kiosk mode. When you’re deploying hundreds or thousands of screens across locations, the economics of Android vs. Windows licensing stack up fast.

Why Android overtook Windows for new kiosk deployments

The installed base still has a lot of Windows — legacy systems from the 2010s built on Windows 7/8/10 IoT by manufacturers like NCR and Diebold Nixdorf. But the new deployments tell a different story.

What pushed Android ahead:

- Zero licensing cost. Android is open-source. Windows IoT carries per-device licensing fees that compound across large deployments. For a chain rolling out 500 kiosks, that difference runs into six figures.

- Lower hardware requirements. Android runs smoothly on ARM-based processors and embedded chipsets that cost a fraction of the x86 hardware Windows typically needs. Faster deployment, cheaper total build.

- Mature app ecosystem. Millions of Android developers globally. Businesses can build custom kiosk apps, integrate payment gateways, connect loyalty programs, or deploy content management — all within a familiar development environment.

- Cloud-native device management. Android Enterprise, Google’s dedicated device management framework, lets operators lock devices into kiosk mode, push updates remotely, and monitor fleets from a centralised dashboard. No on-site maintenance visits for routine updates.

- Hardware diversity. Android runs on everything from compact tablets to large-format displays to android-based interactive kiosk systems with integrated payment modules, receipt printers, barcode scanners, and NFC readers. That flexibility lets manufacturers design for specific industries without being locked into one hardware tier.

Windows still dominates where complex multi-peripheral setups are needed — banking terminals with biometric scanners, or legacy POS integrations that were built around Windows APIs. But for the fastest-growing segments — QSR self-ordering, retail self-checkout, hospitality check-in, healthcare registration — Android is where the new money goes.

The self-service market is growing at double digits across every major vertical

Quick breakdown of where self-service kiosks are expanding fastest:

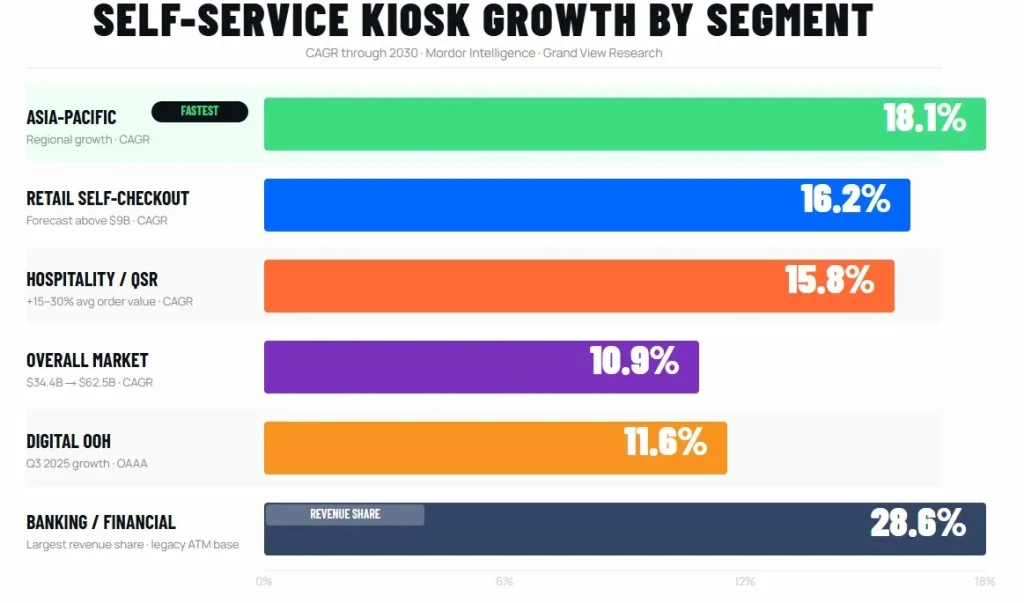

- Retail self-checkout is the fastest-growing segment at 16.2% CAGR through 2030, forecast to climb above $9 billion (Mordor Intelligence).

- Hospitality and QSR expanding at 15.8% CAGR — self-ordering kiosks in restaurants increase average order values by 15-30% through automated upselling and visual menus (KioskIndustry.org).

- Healthcare registration accelerating as providers digitise front-desk workflows. Kiosks handle patient check-in, insurance verification, appointment confirmation, and wayfinding.

- Banking and financial services still held the largest single-segment share at 28.6% of kiosk revenue in 2024 — but that’s legacy ATM and branch infrastructure, not high-growth.

- North America accounts for roughly 33-39% of global kiosk revenue depending on source, with Asia-Pacific growing fastest at 18.1% CAGR through 2030.

The global installed base sits at an estimated 8 to 15 million kiosk units worldwide as of 2025 (TIG – The Industry Group). The broader self-service technology ecosystem — including kiosks, payment terminals, software platforms, and services — exceeds $150 billion globally.

US OOH ad revenue hit a record — and digital screens are the growth driver

The Out of Home Advertising Association of America (OAAA) reported $2.13 billion in Q3 2025 revenue — the highest Q3 on record. Digital out-of-home (DOOH) grew 11.6% in that quarter, making it the strongest growth category. That marks 18 consecutive quarters of OOH growth.

Nielsen projects US retail media spending — which includes endcap screens, checkout displays, and in-store kiosks — to reach $60 billion in 2025 and $100 billion by 2028. Programmatic DOOH is expected to hit $1.23 billion by 2026 as advertisers shift toward real-time, data-triggered placements.

This ad revenue growth directly benefits Android-based display networks because:

- Programmatic ad delivery requires cloud-connected screens — Android’s native cloud management handles this natively.

- Real-time content triggers (time of day, foot traffic patterns, weather, inventory levels) need lightweight OS overhead — Android handles contextual switching without the resource demands of Windows.

- Advertisers want measurement — screen-level analytics, impression counting, audience verification. Android kiosk platforms integrate these through standard APIs.

The portable display trend is pushing Android into temporary and event spaces

Fixed kiosks and wall-mounted signage cover permanent retail installations. But a growing segment needs screens that move — pop-up shops, trade shows, seasonal retail, outdoor events, temporary brand activations.

Portable smart TV solutions running Android fill this gap. Battery-powered or easily relocated displays that connect to the same cloud CMS as permanent installations. A brand can deploy screens at a weekend event, push content from the same dashboard they use for their permanent retail locations, and pull the hardware out Monday morning.

This flexibility is why the kiosk and display conversation is expanding beyond fixed installations. The commercial display market is merging fixed, portable, and interactive formats into one managed ecosystem — and Android’s lightweight, hardware-agnostic architecture sits at the centre of that convergence.

What’s coming next

A few directions worth watching in the second half of 2026:

- AI-driven personalised kiosk content. Screens that adjust recommendations based on time of day, queue length, or anonymised audience demographics. Already piloting in QSR and retail.

- Touchless interaction expanding. QR code scanning, voice input, and gesture control reducing physical contact with shared screens. Accelerated post-pandemic and now becoming standard in healthcare and food service.

- Samsung’s glasses-free 3D spatial signage. Announced for retail and billboard applications — 3D product visuals without wearable hardware. Early stage but signals where the next investment wave goes.

- Retail self-checkout kiosks projected above $9 billion within the current forecast window, driven by grocery chains and mass merchants deploying Android-based systems at scale.

The underlying shift is straightforward. Businesses need interactive screens that are cheap to deploy, easy to manage remotely, and flexible enough to run custom apps across different industries. Android checks every box. The market data confirms it. And the pace of deployment is accelerating, not slowing down.

References

- Verified Market Research, “Kiosk Operating System Market” — Android holds largest segment share.

- Maximize Market Research, “Kiosk Operating System Market – Global Industry Analysis and Forecast (2025-2032).”

- KioskIndustry.org, “Which OS to Use in My Kiosk for Better Performance,” December 2025 — Android estimated at 35-45% of new kiosk shipments.

- Grand View Research, “Self-Service Kiosk Market Size, Share | Industry Report, 2030” — $34.4B in 2024, projected $62.5B by 2030 at 10.9% CAGR.

- Mordor Intelligence, “Self-Service Kiosk Market Size & Forecast 2025-2030” — $14.5B in 2025, retail self-checkout growing at 16.2% CAGR.

- TIG – The Industry Group, “Self-Service Technology Statistics 2026” — 8-15 million global installed kiosk base, $150B+ broader ecosystem.

- OAAA, Q3 2025 OOH Revenue Report — $2.13B, highest Q3 on record, 18 consecutive growth quarters.

- LG Electronics, ISE 2026 booth showcase, February 2026 — via TechRadar.

- Nielsen, US Retail Media Spending Projections — $60B in 2025, $100B by 2028.